LPT, or Local Property Tax, is a self-assessed tax charged on the market value of residential properties in the Irish State .

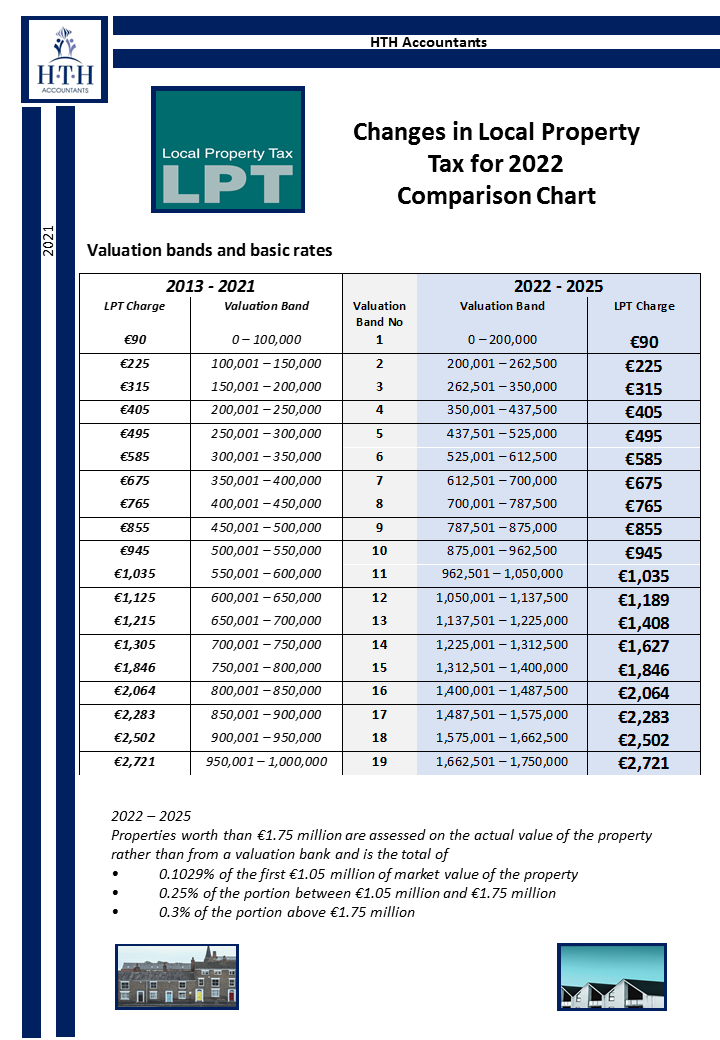

The first LPT valuation period started on 1 July 2013 and will end on 31 December 2021. The Valuation Date for the next four year, which will determine the amount of LPT you pay for 2022 and for the three years from 2023 to 2025, will be based on your valuation of your property as of 1st

November 2021.

LPT is a self-assessment tax so you calculate the tax due based on your own assessment of the market value of the property. Revenue does not value properties for LPT purposes but provides guidance on how to value your property. Revenue will contact you directly this month with information regarding the steps you will need to take. Then, you submit your valuation by 7 November and arrange to pay the tax.

Are you ready for the LPT Valuation Date?

To help you prepare to meet your obligations as a home-owner, here are the steps you should take.

- Determine the value of your property as at 1 st November 2021

- Submit this valuation along with an LPT Return to Revenue by 7 th November 2021

- Pay or make arrangements to pay your LPT for 2022

LPT Exemptions

Certain properties are exempt from paying LPT. Even if you own an exempt property, you must still value your property and make a Local Property Tax return to claim an exemption.

- Properties unoccupied for an extended period by an ill or infirm liable person

- Properties bought or adapted or built for use by incapacitated persons

- Properties certified as having pyritic damage

- Properties constructed using defective concrete blocks

- Properties fully subject to commercial rates

- Properties used by a charity or a public body providing special needs accommodation

- Properties owned by charities for recreational activities

- North-South implementation bodies

- Registered nursing homes

Who should Pay?

If you are the owner or joint owner of a residential property on November 1st 2021, then you are liable for LPT, even if you do not live at that property. If there is more than one owner, or it is owned by a company or other entity, you need to agree who will pay the tax, otherwise Revenue can

collect it from any of the owners.

In some cases, you must pay the LPT if you are not the owner:

- If you are a tenant with a long-term lease of more than 20 years or

- If you have a right to live in the property for life or for more than 20 years or a right to live there ‘to the exclusion of others’

(The landlord pays LPT if a property is rented on a normal short-term lease (less than 20 years).)

How to Value your Property

Standardised guidelines may not reasonably reflect the value of your own property. It is important that you also consider the specifics of your own property. Your property may have certain unique features that you should take into account when determining its value (extensions, additional

features etc.)

You should keep a copy of any information sources and supporting documentation that you use to determine the market value of your property. Revenue may request this from you in the event of a

review of your self-assessment of your property’s value.

Interactive Valuation Tool

Revenue have an interactive valuation guide to help you determine the value of your property. The site shows a map, divided into different small areas. (These are areas that have been complied by the National Institute of Regional and Spatial Analysis on behalf of Ordinance Survey Ireland in consultation with the Central Statistics Office.) There are approximately 18,600 small areas with usually 50 – 200 properties in each, according to property value. Each area is allocated a colour shade for the valuation band. We found this a little difficult to interpret due to the use of single colour shading and recommend using one of the following as additional guidelines.

Other information sources for valuing your property

You can refer to one or more of these information sources to help you make your self-assessment of your property’s value for Local Property Tax (LPT). They are provided here to assist you but Revenue does not endorse or otherwise validate that these sources are valuations for LPT purposes.

Residential property price register

The Property Services Regulatory Authority (PSRA) publishes the Residential Property Price Register. This Register holds information on residential properties purchased in Ireland since January 2010.

You can refer to the Register to check the price of properties that have been sold in your area in recent years. You should compare properties on the Register that are similar to your own property, for example, in type, approximate size and approximate age. You should not rely on one particular sale on the Register, for example, the most recent sale in your neighbourhood. You should consider a group of relevant sales over recent periods.

If the property was a new property when it was purchased, the price shown on the Register is exclusive of Value-Added Tax (VAT). If you are referring to the prices of new properties in your area to determine the valuation band of your own property, you should add VAT at 13.5%.

You should keep a note of the properties on the Register that you use to determine the value of your

own property.

Professional valuation

You may choose to ask a professional valuer to value your property.

The professional valuation should reflect the value of your property on 1 November 2021. The documentation that the professional valuer provides should include the:

- type of property

- size of the property

- condition or state of repair of the property.

Other information sources

You can refer to other available information about properties in your area to help you value your own property. These information sources could include, for example:

- newspapers or other media sources

- information from local estate agents

- commercial property sales websites such as daft.ie, myhome.ie and geowox.com

You should use information about properties in your area that are similar to your own property, for example, in type, approximate size and approximate age. The information you use should be from recent years to help you value your own property as at 1 November 2021.

See the following details from Revenue.ie:

How to correct your property valuation

Your Local Property Tax (LPT) Return, including your self-assessed property valuation, should be submitted to Revenue by 7 November 2021. Your LPT Return applies to the valuation period from 1 January 2022 to 31 December 2025.

You can amend your LPT Return after 7 November 2021 if you determine that you have:

- under-valued your property in your LPT Return

- over-valued your property in your LPT Return

- incorrectly claimed an LPT exemption or payment deferral

or

- not claimed an LPT exemption or payment deferral to which you were entitled

Your LPT liability amount will be recalculated and will replace the original LPT liability amount for 2022 and form the basis for your LPT charge for 2023, 2024 and 2025.

If the LPT liability for 2022 has increased as a result of the correction to the LPT Return, this increased liability will become payable by you immediately and may be subject to interest.

How to correct a property under-valuation

You can revise your property valuation upwards through the online Correct Return service, using your existing login details for myAccount, Revenue Online Service or the LPT online service.

Your revised valuation should reflect the market value of your property as at 1 November 2021. You do not need to revise your valuation if you think your property has increased in value since 1 November 2021. Your valuation on that date determines the amount of LPT you pay each year

during the valuation period from 2022 to 2025.

If you revise your property valuation, as at 1 November 2021, upwards at a later date, your revised valuation will apply to all years in the valuation period. Any additional LPT charge due may be subject to interest.

How to correct a property over-valuation

If you determine that you have previously over valued your property you should contact the LPT Branch in Revenue and request an amendment to your original valuation as at 1 November 2021.

Your revised valuation should reflect the market value of your property as at 1 November 2021. Events or developments after 1 November 2021 cannot retrospectively affect this valuation. For example, you should not revise your valuation if you think your property has decreased in value since 1 November 2021, due to a subsequent general decrease in property prices.

You should include the following information in your request to Revenue to amend your property valuation as at 1 November 2021:

- how the original over-valuation arose

- confirmation of the revised valuation band that you have self-assessed

- documents to support the revised valuation band, to include at least one of the following:

- details of sales of similar properties in your immediate area, for example, from the the Residential Property Price Register or property sales websites such as daft.ie and myhome.ie

- a professional valuation

- house price surveys in your immediate area.

You may also provide photographs of the property which clearly indicate the features that influence a lower valuation than the original valuation you submitted in your LPT Return.

Documentation

All documents you supply should reflect the valuation date of 1 November 2021. You should keep a copy of any information sources and supporting documentation that you use to determine the market value of your property. Revenue may request this from you in the event of a review of your self-assessment of your property’s value.